Paying off a purchase in three monthly chunks at 0% feels more like a plan than a debt. That framing is exactly why the Monzo Flex Card keeps coming up in conversations about digital banking.

Monzo Flex is a buy-now-pay-later product built directly into the Monzo app for UK account holders. Eligible purchases split into three monthly payments at 0% interest, or stretch over six to twelve months with interest applied.

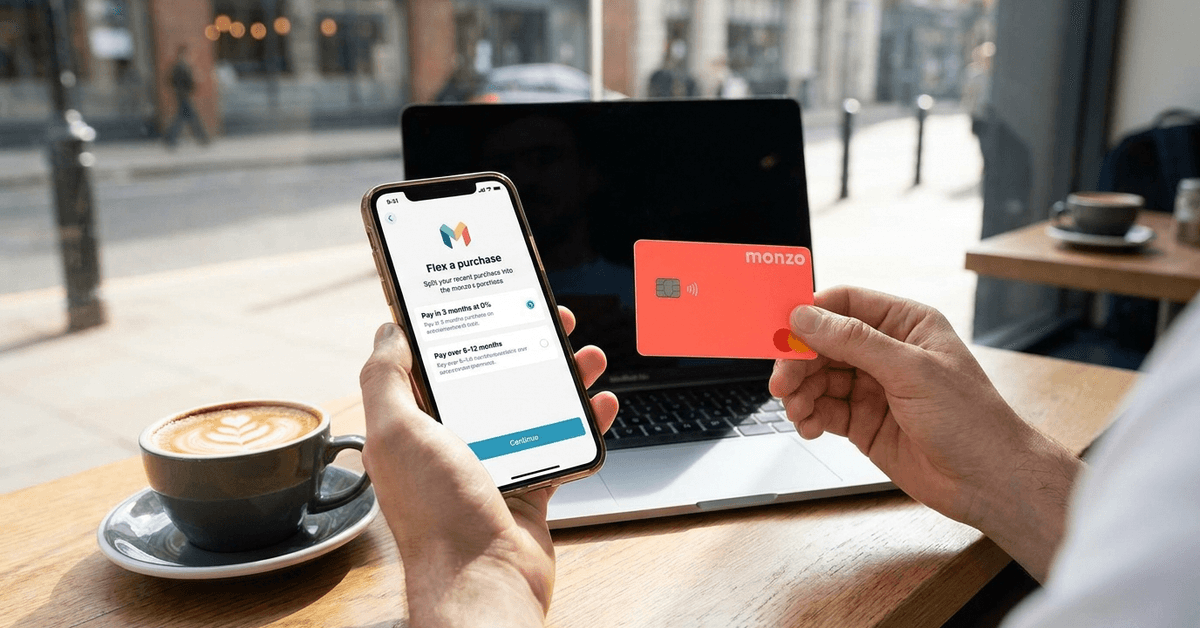

I think the physical card aspect changes the entire comparison with Klarna and Clearpay. Flex is a real Mastercard you tap in-store, not a checkout button that only works at selected online retailers.

This review covers how the card works, where it outperforms competitors, and one situation where I’d stick with a standard credit card over Flex every time.

How the Monzo Flex Card Works as a Physical Card

The single feature that separates Monzo Flex from every other buy-now-pay-later product in the UK: it’s a real, physical Mastercard.

Klarna, PayPal Pay in 3, and Clearpay are checkout buttons at retailers who’ve integrated them. Monzo Flex is a card you tap at a supermarket, a coffee shop, or any physical terminal, and then decide afterward whether to split the payment.

That post-purchase decision is the mechanic worth understanding.

After a transaction appears in the Monzo app, you choose: leave it as a normal payment, split into three monthly installments at 0% interest, or spread it over six to twelve months with interest applied.

Who Can Apply for Monzo Flex

Anyone with an active Monzo account who meets credit and affordability criteria can apply. The approval process is quick, and decisions are usually instant for eligible users.

Once approved, the card is available through Apple Pay or Google Pay before the physical card arrives.

The application triggers a credit assessment, and usage is reported to credit reference agencies. Missed payments affect your credit file, which makes Flex function similarly to a credit card in terms of credit risk regardless of the buy-now-pay-later branding.

Is the 0% Three-Month Split Worth It?

For purchases you can comfortably pay off within three months, the 0% option is a clean deal with no fees attached.

My take on the longer terms: the 6 to 12-month Flex options carry interest and cover a narrower range of merchants than a traditional credit card, which makes them harder to justify if you already hold a 0% purchase card.

The free tier is where Flex earns its place. The extended terms are where you need to do the math first.

What Early Repayment Actually Means

Early repayment carries no penalty. Pay off the balance whenever you want, and interest stops accruing immediately. For anyone who receives a salary payment mid-cycle, this is worth knowing before committing to a longer term.

The Monzo app shows real-time balance updates and all upcoming Flex payments in a single view. That visibility is a real advantage over managing a separate credit card on a different app or banking portal.

Monzo Flex vs Klarna vs PayPal Pay in 3

The buy-now-pay-later space is crowded. The table below shows the clearest differences between the three main options.

| Feature | Monzo Flex | Klarna | PayPal Pay in 3 |

|---|---|---|---|

| Physical card available | Yes | No | No |

| 0% short-term option | Yes (3 months) | Yes (Pay in 3) | Yes (3 installments) |

| Credit reporting | Yes | Yes | Yes |

| In-store use at any terminal | Yes (Mastercard) | Limited | Limited |

| Built into a full bank account | Yes | No | No |

Flex has a structural advantage for anyone who shops in person regularly. Klarna’s edge is its deep integration with online retailers at checkout.

Where Flex Has Real Limitations

Not every merchant category supports BNPL splitting through Flex. Gambling transactions, cash withdrawals, and some travel bookings are excluded from the split option.

For frequent travellers relying on one card for everything, this is a real constraint.

The current list of supported categories is on the Monzo website. Check if a specific spending category matters to you before committing to Flex as your primary card.

Section 75 Protection on Monzo Flex Purchases

This is the angle almost no buy-now-pay-later review covers properly, and it matters for larger purchases.

Under UK consumer credit law, purchases above £100 on a regulated credit product may qualify for Section 75 protection.

This means the credit provider can be held jointly liable if a retailer fails to deliver, goes into administration, or misrepresents a product. Monzo Flex is a regulated credit product. Klarna’s standard BNPL offering typically does not carry this protection.

Splitting a £400 laptop or booking a holiday through a travel agent carries a different level of potential consumer protection on Flex versus Klarna.

The Financial Conduct Authority’s consumer credit guidance covers how Section 75 applies across different credit types, and it’s worth reading if you make high-value purchases regularly.

Checking Coverage Before a Big Purchase

Terms can change. The safest step is confirming Section 75 eligibility with Monzo directly before any large purchase where coverage matters to you. Don’t assume it applies automatically to every transaction.

Who Monzo Flex Is Actually For

The card fits a specific profile. It works well for:

- Existing Monzo users who want credit and a current account managed in one app

- People who shop across online and physical stores and want a single flexible card

- Anyone building a credit history through responsible short-term use

- Shoppers who want 0% short-term credit without applying for a separate credit card

The card is a worse fit for someone who regularly extends payments into six or twelve-month terms. Interest accumulates, and the total cost rises without the broader merchant acceptance of a traditional card.

Practical Tips for Using Flex Without Stress

A few habits that make Flex easier to manage:

- Turn on app notifications so repayment reminders arrive before due dates

- Review upcoming Flex payments weekly rather than monthly

- Limit Flex use to purchases already planned in your monthly budget

- Check the interest rate for any term beyond three months before committing

The spending insights section in the Monzo app makes budget tracking easier, but only if you check it consistently. Passive use of Flex without regular reviews is how balances quietly grow.

Questions People Ask About Monzo Flex

Q: Does applying for Monzo Flex show on your credit file? The application involves a credit assessment that may appear on your credit file. A single check rarely causes a large drop, but multiple applications in a short window can add up. Ask Monzo whether they conduct a hard or soft search before you apply.

Q: Can I use Monzo Flex for purchases abroad? The physical card works at Mastercard terminals internationally, but not all foreign transactions are eligible for splitting. Confirm with Monzo before counting on Flex for a specific travel spending category abroad.

Q: What happens if I miss a Flex repayment? Missed payments are reported to credit reference agencies and can leave a negative mark on your credit file. Monzo sends reminders through the app, so enabling notifications is the simplest way to stay on track.

Q: Is Monzo Flex better than Klarna for purchases above £100? Flex may carry Section 75 consumer protection for purchases above £100, while Klarna’s standard product typically does not include this protection. For high-value purchases where seller default is a realistic risk, Flex has a clear structural advantage.

Q: Does Monzo Flex have a set spending limit? Flex has a credit limit assigned during approval based on your credit history and Monzo account behaviour. The limit varies per user and can be reviewed over time, but Monzo does not publish a standardised cap.

Conclusion

Monzo Flex is a solid choice for existing Monzo users who want short-term 0% credit without a separate card. The physical card format and potential Section 75 protection set it apart from checkout-only BNPL competitors in 2026.

My take is that the 6 to 12-month Flex terms rarely beat a traditional credit card on value. Pull up the Monzo app, check your credit limit offer, and see whether three months interest-free fits your actual budget.