Picking a cash back card sounds simple until you realize some cards demand attention every three months just to unlock their best rates. The Discover it Cash Back card is one of them.

If you are someone who pays vague attention to your credit card rewards but has never bothered to activate a quarterly category, this article is for you. The card’s rotating 5% cash back categories get mentioned in every review.

What those reviews skip is an honest conversation about when the rotation works against you and when to stop pretending you will optimize it.

I think the Discover it Cash Back card is genuinely good for one specific type of person: a household spender who checks their Discover app at least once a quarter and shops at Amazon or grocery stores regularly. Everyone else should probably look elsewhere.

How the Discover it Cash Back Rotating System Works

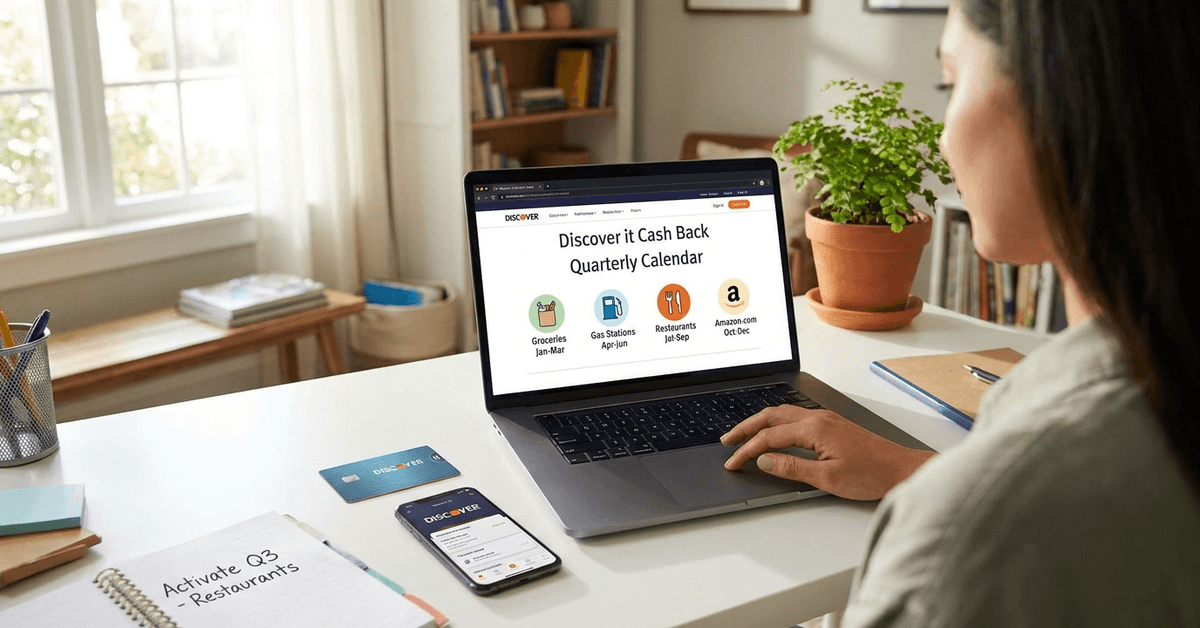

The card earns 5% cash back on rotating quarterly categories, up to $1,500 in purchases per quarter. Every purchase outside that category earns 1%. The math is simple. The discipline required is less so.

Each quarter, Discover announces a new set of bonus categories. Grocery stores, gas stations, restaurants, Amazon.com, PayPal, and digital wallets like Apple Pay or Google Pay have all appeared at various points.

The categories shift every year, so last year’s schedule is a rough guide at best.

Does the Category Calendar Actually Match How You Spend?

A sample of how the schedule has historically looked:

| Quarter | Common Category Examples |

|---|---|

| Q1 (Jan–Mar) | Grocery stores, fitness clubs |

| Q2 (Apr–Jun) | Gas stations, public transit |

| Q3 (Jul–Sep) | Restaurants, PayPal, rideshares |

| Q4 (Oct–Dec) | Amazon.com, Target, Walmart.com |

The Q4 lineup is the one that tends to make cardholders feel good about their choice. Catching Amazon during the holiday season is a real win.

The Q2 gas station quarter is useful for drivers but mostly irrelevant if you work from home. The categories are not random, but they do not bend to your specific spending pattern either.

The Activation Requirement Nobody Talks About Honestly

Quarterly activation is required. Discover does not apply the 5% rate automatically. Log into your account or the Discover app before the quarter ends and activate manually.

Skip it and you earn 1% on everything, including the purchases that were supposed to be earning 5%.

This is where I genuinely disagree with most card reviewers. The standard advice is to “just set a reminder” and treat activation as a minor inconvenience. I think that framing undersells how often real people miss it.

A single missed quarter costs up to $75 in lost bonus cash back. Over a year, that is $300 in foregone rewards for a card that advertises $300 as its ceiling.

The activation requirement is a structural design feature that shifts risk to the cardholder, and reviews should say so plainly.

What You Can Actually Earn in a Year

The math runs cleaner than most people expect.

Spend $1,500 per quarter in the bonus category and you earn $75 per quarter at 5%. Over four quarters, that is $300 in bonus cash back. Add 1% on everything else you spend through the year and the total climbs further.

Then there is the Cashback Match: Discover matches all rewards earned in the first 12 months for new cardholders. One time only. That means the $300 in quarterly bonuses could become $600, plus a match on all your 1% earnings.

For a new cardholder who uses the card actively across all four quarters, a first-year return of $500 to $700 is realistic without extravagant spending.

The table below shows what the quarterly bonus alone looks like at different spending levels:

| Quarterly Spend in Bonus Category | Cash Back Earned at 5% |

|---|---|

| $500 | $25 |

| $1,000 | $50 |

| $1,500 (max eligible) | $75 |

Spending beyond $1,500 in the bonus category earns 1%, same as everything else. The ceiling matters.

When the Math Gets Messy

Not every purchase at an eligible store actually codes as a bonus category. A grocery run at a warehouse club like Costco may not register as a grocery store purchase depending on the merchant category code.

Discover’s own FAQ is the most reliable place to confirm before assuming your spending qualifies. Check the Discover cashback calendar and category details before each quarter begins.

Some superstores and multi-department retailers can fall outside the category even when it looks like they should qualify. This is not unique to Discover, but it catches people off guard when the expected bonus does not show up on their statement.

How Discover Stacks Up Against Chase Freedom Flex and Citi Custom Cash

All three of these cards carry no annual fee and offer elevated cash back rates. The differences come down to structure and effort required.

| Card | Bonus Cash Back Rate | Category Activation Needed | Annual Fee |

|---|---|---|---|

| Discover it Cash Back | 5% rotating, up to $1,500/quarter | Yes, quarterly | $0 |

| Chase Freedom Flex | 5% rotating + fixed categories | Yes, quarterly | $0 |

| Citi Custom Cash | 5% on top spending category, up to $500/month | No | $0 |

The Citi Custom Cash wins on automation. It tracks your highest spend category each month and applies 5% automatically, capped at $500 per month in purchases. No login required. No reminder needed.

My take: the Discover it Cash Back card beats the Citi Custom Cash in raw earning ceiling. $1,500 per quarter at 5% versus $500 per month at 5% means Discover’s quarterly cap is effectively three times higher per month during bonus periods.

But the Citi card removes activation friction entirely, and for people who forget to check their rewards apps, that friction has a real dollar cost.

Redeeming Discover Cash Back: Fewer Complications Than You’d Expect

Rewards can go toward a statement credit, a direct bank deposit, or gift cards. Gift cards occasionally carry a slight bonus: a $25 gift card for $20 in rewards, for example. Those opportunities show up seasonally and vary.

Cash back does not expire as long as the account stays open. Closing the card forfeits any unredeemed balance, which is a detail buried in the terms that surprises more people than it should.

There is no redemption game to play here. No transferring points, no booking windows, no minimum balance thresholds for most redemption types.

The Consumer Financial Protection Bureau’s guide on credit card rewards covers redemption rights broadly if you want a baseline for what card issuers are required to disclose.

A Note on Taxes and Cash Back

Cash back earned on personal spending is generally treated as a rebate by the IRS, so it is not taxable income for most cardholders.

Business spending is handled differently, and those records are worth keeping separate. When in doubt, a tax professional is the right call, not a credit card review article.

Who Should Actually Get This Card

The Discover it Cash Back card rewards a specific habit: quarterly check-ins combined with spending that overlaps with at least two or three rotating categories per year.

Cardholders who benefit most tend to share a few traits:

- They shop at Amazon or major grocery chains regularly, covering Q4 and Q1 historically

- They use digital wallets or PayPal, which have appeared in multiple recent quarters

- They are comfortable logging into a financial app once every three months

People who probably will not get much from it:

- Cardholders who prefer set-it-and-forget-it rewards

- Those whose spending skews heavily toward categories that rarely appear in the rotation (travel, specialty retail, subscriptions)

- Anyone who finds the activation reminder easy to ignore

Questions People Ask About Discover it Cash Back Rotating Categories

Q: What happens if I forget to activate a quarter? Purchases in the bonus category still earn 1%, same as everything else. There is no retroactive activation. Once the quarter passes, the bonus window for that period is closed.

Q: Can I earn 5% cash back on gift card purchases? Discover typically excludes gift card purchases from bonus category earnings, even when bought at an eligible retailer. Check the terms each quarter because the exclusions are listed there and do occasionally change.

Q: Does the Cashback Match apply to the 5% bonus categories? Yes. Discover matches all cash back earned in the first 12 months, including the 5% bonus earnings. A cardholder who earns $300 in quarterly bonuses during year one would see that matched to $600 at the end of the year.

Q: Are warehouse clubs like Costco or Sam’s Club included when grocery stores are the bonus category? Warehouse clubs often have a different merchant category code than standard grocery stores. Discover has excluded them in past quarters, so verifying the category terms before assuming eligibility is worth the two minutes it takes.

Q: Is there a limit on the 1% cash back for non-bonus purchases? The 1% rate applies to all purchases outside the quarterly bonus category with no stated spending cap. Only the 5% bonus earnings are capped at $1,500 per quarter.

Conclusion

The Discover it Cash Back card is a solid no-fee option for cardholders willing to engage with the quarterly system at least enough to activate categories and shop with some awareness.

Skipping activation consistently turns a competitive rewards card into a flat 1% card, which is a poor trade.

For organized spenders who hit grocery stores, Amazon, or digital wallet categories regularly, the first-year Cashback Match alone can make this one of the better-returning cards in the no-annual-fee category.

The card’s structure is built to reward attention, so the only real question is whether you are the kind of person who will give it that.